GOVERNMENT AND ECONOMIC INFLEXION

There’s nothing new about conspiracy theories – we’ve long been invited to believe that the security services assassinated JFK, or that the Moon landing was faked, or that Elvis is alive and well and working in a supermarket somewhere – and most of us have always given short shrift to such claims.

What’s different now is the inter-connected nature of such theories, and traction they continue to gain with the general public. The common theme of such claims is that Western states are ruled by a self-serving clique which daily deceives and schemes against the public for its own nefarious ends.

To be clear about this, we don’t have to believe in such theories in order to take them seriously. At the very least, they are destabilizing, and corrosive of trust.

This undermining of faith in the integrity of government has been happening at the worst possible time, with the economy inflecting from growth into contraction, a ‘GFC II’ financial crisis looming, and a very real environmental and ecological crisis unfolding.

Ideally, governments would be addressing these issues in search of constructive responses centred on the good of the public as a whole, and the governed would be placing trust in the honesty and intentions of the governing.

In fact, the very opposite has happened, and we need to try to work out why.

The best way to do this is to concentrate, not on the distractions of party politics, still less on the politics of personality, but on the way government is and has been conducted, particularly in the West.

Economics aren’t everything in government, but aren’t very far off. People enjoying prosperous lives, in a society whose fairness they trust, are very unlikely revolutionaries. Hardship, and perceptions of unfairness and dishonesty, are the stuff of which political instability is made.

From this perspective, the ‘establishment’ – or whatever term we choose to apply – has two very big problems. First, their routine assurances that economies are continuing to grow are being falsified by events. Second, their behaviour during and after the 2008-09 global financial crisis was inexcusable.

These two issues are intimately connected. By the second half of the 1990s, in a process known at the time as “secular stagnation”, economic growth was decelerating very markedly. The proposed ‘fix’ was credit expansion, which didn’t re-energise the economy (because it couldn’t), but did lead straight to a very serious financial crisis.

In a sense, the adoption of credit adventurism was ‘the break-in’ in this economic version of Watergate, and the response to the GFC was ‘the cover-up’, and the latter did a lot more damage than the former.

As the banking sector teetered on the brink in 2008-09, the authorities made two big calls. First, they would engage in unorthodox, ultra-loose monetary policies, centred on QE, ZIRP and NIRP. Second, they would promise the public that these were “temporary” expedients, to be kept in place only for the duration of the “emergency”.

We need to be in no doubt at all about what these policies did. First, they were a gigantic exercise in moral hazard. Second, they handed enormous gains to some at the expense of others. Third, they abrogated the principles of market capitalism.

By moral hazard is meant the sending of dangerous signals. What should have happened during the GFC was what had happened in previous financial crises – those who had been reckless, or were simply unlucky, would be wiped out, the system would dust itself off, and normality would return.

But rescuing dangerously overindebted businesses and individuals sent the message that, should similar conditions recur, they could expect to be rescued again. This took off the brakes on all kinds of excess risk.

Worse still, the extreme tools used to rescue the reckless at the expense of the prudent handed enormous unearned gains to (generally older) people who already owned assets, at the expense of (generally younger) people who aspired to find rewarding careers and start to accumulate capital.

Third, these enormous interventions destroyed the essential principles of market capitalism. In a market system, the possibility of taking big losses is a necessary corrective to the pursuit of profit. If rescuing the reckless wasn’t bad enough in itself, ultra-low rate policies made it impossible for investors to earn positive real (above inflation) returns on their capital. The markets were prevented from carrying out their essential functions, which are price discovery and the pricing of risk.

Perhaps my memory is at fault, but I can’t recall being given an opportunity to vote on a programme of rescuing the reckless, handing enormous unearned capital gains to a favoured few, or scrapping the basic precepts of market capitalism.

Things mightn’t have been quite so bad if the authorities had kept their promise about these expedients being “temporary” fixes for the duration of the “emergency”, but these policies were kept in place for a period longer than the combined lengths of the first and second world wars.

Instead of conveying an impression of competence in an emergency, the handling of the GFC sent the message that, when a crisis arises, the instinctive response of the authorities is to take care of the wealthy and the well-connected, and leave everyone else to take their chances.

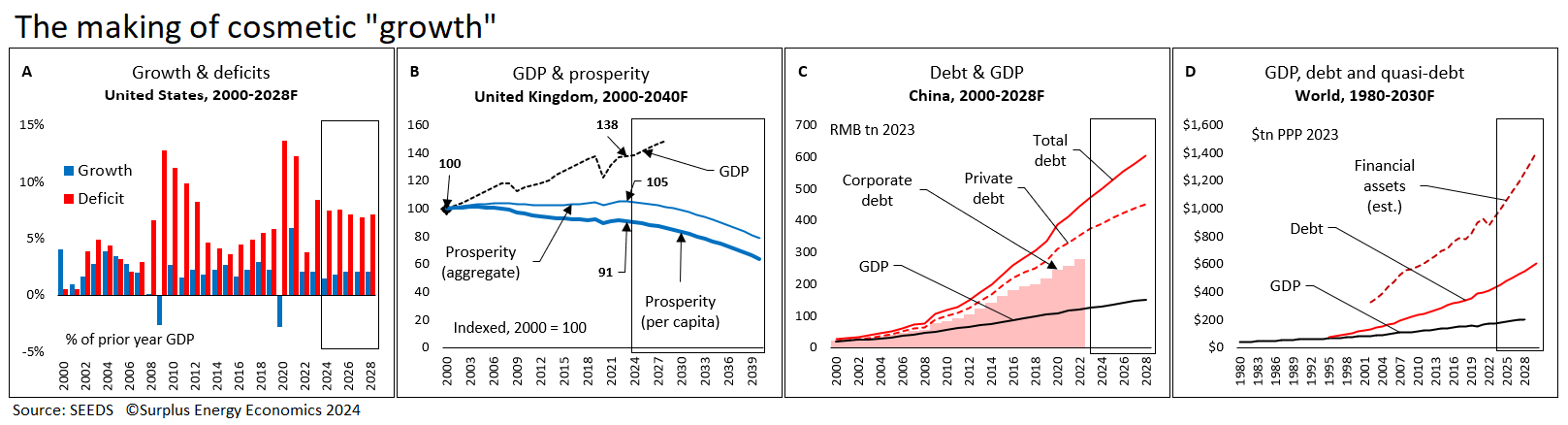

Having blown this enormous hole in their credibility, the authorities are reduced to giving assurances that cannot be believed. They insist that “growth” is continuing, a claim which is put in context in the following charts. A 2% rise in real GDP isn’t “growth” if the government has to borrow 8% of GDP to make it happen. There’s no point in rival politicians promising “growth” in a country whose prosperity hasn’t grown in fifteen years, and whose social infrastructure is falling to bits. We can’t build long-term economic “growth” on a real estate Ponzi scheme.

The only thing that’s really growing now is the World’s gigantic burden of debt and quasi-debt.

The great hope now is, supposedly, technology, which has become the secular faith of the modern age. Sometimes abbreviated “tech”, this is going to re-energise the economy, save us from environmental disaster, and carry on making vast profits for those invested in it.

Ultimately, technology is a vast exercise in collective hubris, a statement that human ingenuity can rule the universe.

The reality, of course, is that our powers are much more circumscribed.

No amount of ingenuity can deliver material resources that don’t exist, or repeal the laws of physics to deliver infinite economic growth on a finite planet.

Some technologies are already failing. We can no longer operate commercially viable supersonic aviation, or put a man on the Moon. We can’t, as our predecessors did, handle waste water without pouring raw sewage into our rivers and seas. We’re already starting to lose faith in some much more recent examples of world-changing technological wizardry.

In an ideal world, the powers that be would admit that economic growth has gone into reverse, and apologise for the monetary gimmickry maintained for more than a decade after the GFC.

This won’t happen, of course. The authorities may not know about the inflexion from growth into contraction, though this is hard to believe. They may have slipped into the trap of – as one senior politician said of another – “believing your own press releases”. They may be following the old adage of ‘don’t announce a problem until you can announce a solution’.

In the absence of constructive policies for managing economic contraction, we’re in for a set of one-at-a-time discoveries. These are going to include discretionary contraction, a financial crisis bigger than that of 2008-09, and the realisation that technology, far from putting us in control of the universe, can’t even carry on making big money.

Through all of this, the social good of trust between governing and governed is likely to become ever more elusive.