TWO ECONOMIES, ONE PROBLEM

Inflation isn’t like other economic problems.

It impacts the general public, immediately, and painfully. It feeds on itself, once wages start chasing surging prices.

It can’t be denied and, once it takes off, there are limits to how far it can be under-reported. It can’t be fixed – or, rather, it can’t be ‘kicked down the road’ – using any form of ‘magic money’ gimmickry.

Inflation is the brutal exposer of failure. It is already exposing, for example, the weaknesses of a British economic model built on perpetual credit expansion, and the contradictions in a European monetary system which tries to combine a single monetary policy with nineteen sovereign budgetary processes.

Small wonder, then, that soaring inflation induces panic, desperation and sometimes outright idiocy in the corridors of power.

On the basis of principle

Those of us who understand the economy as an energy system, rather than a wholly financial one, have a unique insight into inflation.

Because we recognize that the ‘real’ economy of goods and services is shaped by energy rather than by money, we also recognize the existence of the ‘financial’ economy as a monetary proxy to the energy dynamic which determines prosperity.

Prices are where the material and the monetary intersect. Prices are the financial values that are attached to physical goods or services. Inflation is a product of changes in the relationship between the ‘real’ economy of energy and the ‘financial’ economy of money and credit.

To paraphrase Milton Friedman, inflation is always and everywhere a two economies phenomenon.

Because of the immediacy of soaring inflation, and because of the panic it induces in decision-makers, current events might seem to add credence to the “collapse” prophecies of modern-day Cassandras.

In fact, inflation can be interpreted rationally, and that’s the single aim of this discussion.

In search of reason

The basic principles of the energy interpretation are quickly stated.

The economy is an energy system, because nothing that has any economic value at all can be supplied without the use of energy.

Energy is never ‘free’, but comes at cost measurable as the proportion of energy that is consumed in the access process whenever energy is accessed for our use. This ‘consumed in access’ component is known here as ECoE (the Energy Cost of Energy).

Money has no intrinsic worth but commands value only as a ‘claim’ on the material goods and services supplied by the energy economy.

These principles lead inescapably to the concept of the ‘two economies’ of energy and money. Inflation – and, for that matter, currency crises, market falls and severe defaults – are products of imbalances between the ‘real’ and the ‘financial’ economies.

Until some point in the 1990s, the real and the financial economies expanded more or less in tandem.

The most notable previous disequilibrium between the two economies of energy and money happened in the 1970s, and was characterized by runaway inflation. Though energy remained cheap and abundant in those years, political divisions between the biggest producers and the main consumers of oil triggered a sharp rise in the cost of energy to Western consumers.

The situation righted itself, because there remained substantial reserves of relatively low-cost oil in places – most notably the North Sea and Alaska – that were outside the control of OPEC.

The robust growth of the 1980s owed everything to a ‘catch-up’ from the politically-induced energy shortfalls of the 1970s, and almost nothing to the ‘liberal’ economic ideologies which happened to supplant the Keynesian orthodoxy at that same time.

The road to here

By the 1990s, the fundamentals had started to deteriorate. ECoEs were rising at rates which were taking away the potential for further growth in the material economy. This was happening because of depletion, a process whereby lowest-cost energy resources are used first, leaving costlier alternatives for a ‘later’ which had now arrived.

What we have experienced since then has been a worsening process of self-delusion, based on the false proposition that we can increase material supply by stimulating financial demand.

The facts of the matter, of course, are that no amount of financial stimulus, and no increase in prices, can produce anything – in this instance, low-cost energy – which does not exist in nature.

What we can do is to create a simulacrum of “growth” by creating monetary ‘claims’ on the future which increase transactional activity in the present.

We’re at liberty to count these increases in transactional activity as ‘growth’, and to ignore the inability of the real economy to honour these forward commitments when they fall due.

This is what’s been happening through an era of collective self-delusion that began in the second half of the 1990s.

Between 1999 and pre-pandemic 2019, reported global GDP increased by $74 trillion in real terms, but debt escalated by $204tn between those years, and we can estimate that broader ‘financial assets’ – which are the liabilities of the household, government and corporate sectors of the economy – soared by about $480tn. Even this number excludes the creation of enormous pension promises which a faltering ‘real’ economy will be unable to honour.

The reported “growth” in the economy measured financially as GDP through this period was starkly at odds with what was happening in the real economy of energy. Whilst reported GDP slightly more than doubled (+110%) between 1999 and 2019, the total supply of energy increased by only 54%, a number that falls to 47% at the critically-important level of ex-ECoE surplus energy.

Reflecting this, aggregate prosperity, measured financially by the SEEDS economic model, expanded by only 34% worldwide over a period in which economic activity, recorded as the transactional use of money, rose by 110%. The 34% increase in money-equivalent prosperity was lower than the 47% rise in surplus energy, a differential reflecting deterioration in the efficiency rate at which surplus energy is converted into economic value.

The dynamics of disequilibrium

We need to be absolutely clear about what this means. Stimulation of transactional activity to levels far above underlying prosperity as determined by energy has created an enormous disequilibrium between the ‘real economy’ of goods and services and the ‘financial economy’ of money and credit.

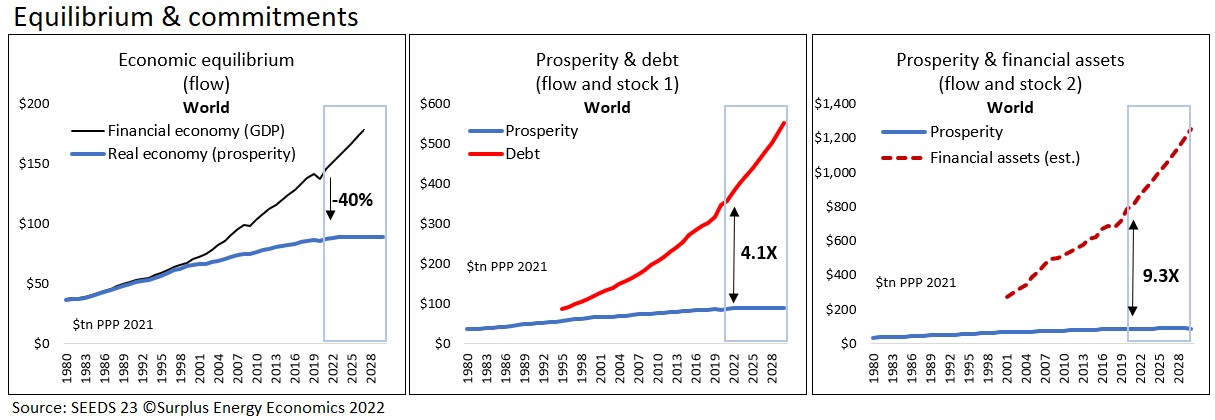

Globally, the downside between the ‘two economies’ can be calculated, as of the end of last year, at 40% (see fig. 1). The equivalent numbers for the United States and China, respectively, are 32% and 54%.

Fig. 1

The inevitable restoration of equilibrium between the ‘two economies’ is readily explained, because it happens when the owners of financial ‘claims’ realize that the aggregate of these claims cannot be honoured ‘for value’ by the real economy of goods and services.

This enforced restoration of equilibrium is mediated through prices, which are best understood as the rate of exchange between the monetary and the material economies.

The result is experienced as accelerating inflation, a process which everyone understands can only be worsened by stimulus, and which we further understand must continue until something much closer to equilibrium has been restored.

It also follows, from this, that inflation will be most acute in those energy-intensive product categories which are ‘essential’, which means that consumers cannot choose not to buy them because their prices have increased.

Conversely, inflationary pressures will be less pronounced in those discretionary (non-essential) goods and services of which consumers will reduce their purchases as their ex-essentials prosperity (known in SEEDS as PXE) deteriorates.

Taking stock

This explanation, though, refers primarily to the flows of money and material prosperity. There are also ‘stock’ issues around the forward commitments created through the same process of stimulus which has driven the observable wedge between the ‘real economy’ of goods and services and the ‘financial economy’ of money and credit.

This is summarised in the flow-and-stock analysis produced by the SEEDS economic model.

In fig. 2, the flow distortion, seen earlier, is compared with two measures of ‘stock’ exposure. One of these is debt, which now stands at 4.1X underlying prosperity. The other relates to estimated broader financial assets, now at a multiple of 9.3X prosperity.

Neither of these ratios is sustainable, and a best estimate has to be that forward excess claims will be eliminated at a percentage rate broadly equivalent to the equilibrium downside measured as the flow relationship between the monetary and the material economies.

Fig. 2

Inflation does, of course, reduce forward claims by impairing their real value.

Even so, the balance of segmental alignments – between essentials, discretionaries and capital investment – suggests that the elimination of excess claims cannot occur through inflation alone. Suppliers of essentials probably will be able to honour most of their forward commitments, whilst many discretionary sectors will not.

Since our focus here is on inflation rather than on economic activity and prosperity, we need, for now, only glance – as in fig. 3 – at the future prospects for an economy in which prosperity has stopped expanding and started to contract, whilst the real costs of essentials carry on rising.

Discretionary activities will shrink, whilst capital investment can be expected to diminish in a process that demands ever greater returns on capital.

On inflation, our conclusion needs to be that pressures will continue for as long as it takes for the restoration of equilibrium between the ‘real economy’ of energy, goods and services and the ‘financial economy’ of asset values, money and credit.

Within this overall trend, the prices of essentials will continue to out-pace those of discretionaries as the segmental mix of consumption and investment realigns.

For the authorities, this poses a difficult challenge, because many emerging trends will be unpalatable to a public which has been sold the myth of ‘growth in perpetuity’.

Whilst we can – perhaps – assume that no government or central bank would be so unwise as to try to use stimulus to counter inflation, there are two ways in which the authorities could make this worse.

One way would be to carry on trying to ignore, or unintentionally misunderstand, the forces that are manifesting as inflation.

The other would be to try to favour some interest groups over others.

Fig. 3